Observations and perspective on the effect of the cost cap provision on carbon and rate outcomes in reaching 100% GHG-free electricity by 2045.

Summary

The 100% Clean Electricity bill (SB 5116) includes a cost cap intended to limit the risk of rate increases to utility customers. The cost cap also provides system engineers a specific target to use in their planning, i.e. a “Design for Cost” scenario. Compared to an uncapped base case, the cost cap is likely to throttle the avoided greenhouse gas (GHG) emissions into the 2030s. CaPI projects by using a 2% per year rising cost cap assumption utilities will achieve 70% to 95% of the emissions reductions compared to the uncapped case, and by using a stepwise rate increase utilities will achieve 50% to 70%. While there is a strong likelihood of 2030 emission reductions being throttled back to some degree, the impact of the cost cap is expected to be much lower, or null, on utilities reaching at least 99% GHG-free by 2045.

The net effect of the cost cap appears to be extending the timeline for utilities to meet the shorter term 2030 target of 80% clean delivered electricity, without compromising the overall outcome of a near 100% clean system in the year 2045. As with previous analysis, we highlight the 99% GHG-free case rather than the 100% GHG-free case because of the large increase in uncertainty around added costs to go from 99% to 100% GHG-free.

Cost Caps Now Part of SB 5116

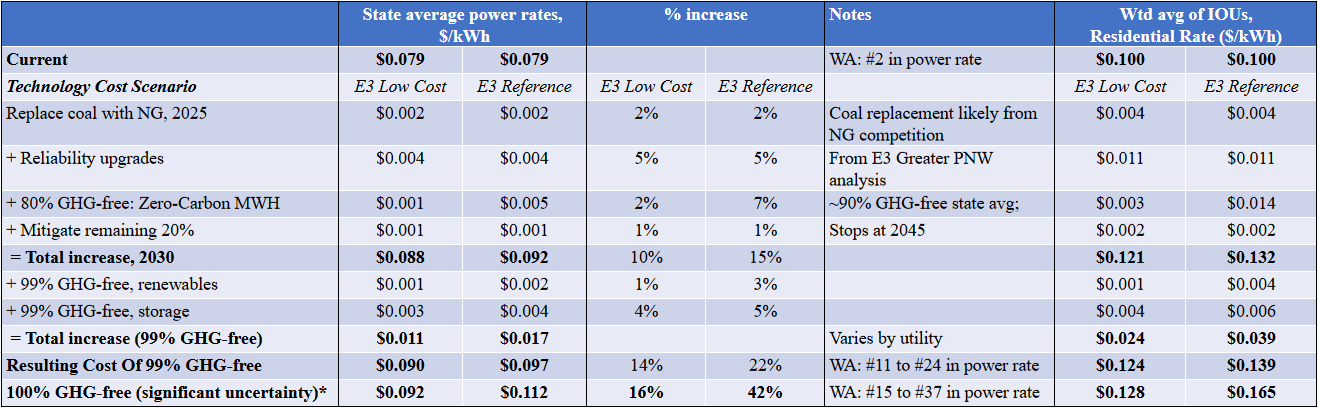

Prior work. We previously reported projected rate impacts of the steps leading to 100% Clean Power – the summary table of which is shown below. Costs shown are as-incurred, aggregated across the full system. Results are shown both state-wide and for Investor-Owned Utility (IOU) residential rates.

Table 1: Summary of 100% Clean Expected Rate Impacts

*Includes CaPI factoring of 99% → 100% GHG-free case

*Includes CaPI factoring of 99% → 100% GHG-free case

The specific language regarding the cost cap is subject to change as the bill moves through the process. Notably, the version as passed the Senate included a cost-cap rising at 2% per year, and a subsequent House Committee amendment changed the cost-cap to be averaged over an eight-year period relative to a 2% annual cost increase.1 At a public hearing of the House Finance Committee on March 21st, legislators and stakeholders suggested that an eight year could be reduced to a four-year average for greater consistency with the compliance period proposed in the bill.

The cost cap is only applicable to bill requirements from 2030 onward – the 80% GHG-free generation plus mitigation of remaining GHG-emitting generation in 2030 progressing to 100% GHG-free generation by 2045. Interim targets between 2030 and 2045 would also be set and subject to the cost-caps. There is no cost cap provision for eliminating coal from electricity rates.

We applied two assumptions of cost cap design to our 100 Percent Clean model in order to test expected carbon reduction and cost-effectiveness impacts. Based on our reading of the bill language as well as consultation with key stakeholders, we project costs will begin rising in 2023. This coincides with the specific date for interim targets to be in place.2

A 2% per year increase starting in 2023 aggregates to a maximum 17% rate increase in 2030, and a maximum 58% rate increase in 2045. Under an eight-year averaged rate increase, one possibility is step-wise increases in rates spaced out every eight years with investments front-loaded: a 9% increase in 2023, rising to a 19% increase in 2031, and finally a 30% increase in 2039. Again, the rate-impacts are above the rate impacts of eliminating coal. These price trajectories are shown in Figure 1 (dashed lines: blue = Linear, black = Step Averages), alongside the projected statewide average rate increases with no cost cap as detailed in our prior analysis (solid lines). The no-cap cost increases charted alongside IOU residential rates are shown in Figure 2.

Figure 1: Cost caps proposed in SB5116 along with projected, average statewide rate increases

Figure 2: Cost caps proposed in SB5116 along with projected, average rate increases for IOU residential customers

How do the cost caps project to change outcomes?

Regardless of the cost cap, all coal is required to be eliminated by 2026, setting the initial “weather-adjusted sales” (for IOUs) or “retail revenue requirement” (for Customer Owned Utilities, “COUs”), against which a cost cap would be determined. Those costs were projected to add 0-10% to rates (though only over 3% for one utility) above a scenario with only pre-existing policies in effect.

We estimate that the outcome of coal elimination (beyond already announced or negotiated closures) replaced with natural gas is 4.1 million metric tonnes of carbon dioxide (4.1 MtCO2) per year at a cost of $16 per coal-MWh or $36/tCO2.

Full data-tables for cost cap impacts on the 2030 and 2045 outcomes, refer to the Appendix.

Carbon and cost impact in 2030

Uncapped

The cost-cap in 2030 is higher under a 2%/year increase than a step-wise average – although they temporarily synch up in 2031. The bills clearly state that for cost-cap purposes, the 80% GHG-free standard achieved by new resources and conservation must be satisfied before a utility can rely on offsetting emissions. As in the original analysis, we assume that solar backed with infrequently run gas peakers are deployed first. Offset purchases are assumed to the extent that they can be without exceeding the cost cap (see documentation of original analysis).

Without cost-capping, the transition to at least 80% GHG-free for each utility, while not increasing the GHG-emitting share of any utility, is projected to avoid 5.4 MtCO2 annually starting in 2030. The cost of reducing this carbon is roughly $20-$90/tCO2 for renewables plus another $74/tCO2 needed for system reliability, up to a total of roughly $90-$170/tCO2. To the extent that new resources for backing renewables and increasing system reliability are not needed or are needed eventually but not by 2030, the cost per unit of carbon avoided would scale downwards and/or shift to later.

Additional offsetting of GHG-emitting generation reduces another 4.1 MtCO2 annually – assuming quality offsets can be purchased at a cost of $24/tCO2 (assumed equivalent to $10/MWh). The total annual cost beyond eliminating coal is projected to be $0.6 to $1.0 billion per year – an average rate increase of 7% to 11%. Rate increases would be higher for IOUs and lower for COUs in general. Once coal is eliminated, the average cost of avoided carbon in 2030 projects to $65-$105/tCO2. Combined with the 4.1 MtCO2 reduced from transitioning coal to natural gas, the total impact in 2030 projects to be 13.6 MtCO2 at a cost of $55-$85/tCO2.

Effect of cost cap in 2030

Under a 2% annual increase, maximum cost increases total over 17% by 2030, and anywhere from one to three of the IOUs are expected to reach the cost cap before achieving 80% GHG-free generation. The net impact on emissions is roughly 4.0 to 5.4 MtCO2 avoided in 2030 from new renewables plus 1.3 to 3.7 MtCO2 offset.

Including elimination of coal generation, 70% to 97% of the uncapped scenario emissions reductions are projected to occur with a 2% rising cost-cap that starts rising in 2023.

This capped scenario projects to a statewide 85-90% GHG-free system in 2030 with roughly one-third to ninety percent of the remaining emissions offset. Costs to achieve these reductions are roughly $600 to $700 million per year, in addition to the nearly $150 million per year estimated for transitioning off the remaining coal by 2026. Translated to costs per avoided ton of carbon, costs are roughly $70-$130/tCO2 for avoided emissions above and beyond coal closure, or $60-$90/tCO2 when including the initial transition away from coal.

How does that translate to rate increases? Once the rate increases of transitioning away from coal are assumed (1.6% statewide, 3.8% for IOU residential customers), rates project to increase by around 7% state-wide and by about 16-17% for IOU residential customers.

By comparison, a step-wise rising cap would increase costs by over 9% for 2023 through 2030, before roughly doubling in 2031. One impact of the step-wise approach is likely earlier deployment of zero-carbon resources, creating a strong likelihood of additional carbon reductions in the mid-2020s relative to the 2% per year increasing cost-cap. Carbon reduction results could also jump in 2031 as the cost-cap again rises. Given a lower cost cap under from 2031-2045 (Figure 1), the cumulative carbon reduction would be expected to be lower for the rest of the program period, all else being equal.

Using a 9.4% cost-cap scenario in 2030, avoided emissions project to 2.3 to 3.7 MTCO2 from renewables plus 0.9 to 1.3 MTCO2 from offsets. Including the emissions reductions from transitioning off coal, annual avoided carbon is 50-70% of the total with no cost-capping. Annual costs of roughly $400 million per year translate to a range of $75-$125/tCO2 avoided. With the additional costs and carbon reduction from the coal transition, total costs of reducing carbon in 2030 project to $60 to $75/tCO2. This provides one possible scenario for how an eight-year average of costs could be applied, with front-loaded investments paid back in rate increases for eight-years.

In terms of rate-increase, statewide average rates in 2030 project at roughly 5% higher while residential IOU rate increases project at nearly double that. Both carbon reduction and rates would be anticipated to increase step-wise again in 2031 under this scenario.

Effect of cost cap in 2045

We’ve decided to add a 99% GHG free case in 2045 to the analysis because of the potential complications of achieving 100% Clean Power with renewables as the primary generation source (see original analysis). The uncapped avoided emissions of going from 80% to 99% GHG-free generation, relative to a baseline where natural gas generation is added to meet load growth, is 12.2 MtCO2 of avoided carbon at an incremental cost of $400 to $800 million per year. This translates to $34-$64/tCO2. Note that some of these avoided emissions replace what was previously required as offsets under an 80% GHG-free plus mitigation to carbon neutral requirement for 2030.

With costs caps in place, maximum 2045 cost increases are 58% under a linear approach and 31% for a stepwise approach. A linear approach projects to at least very nearly meet the uncapped case: even under the higher-cost scenario we project 98% of the reduction as the uncapped case. Incremental costs range from $400M to $1 billion (includes extra costs of getting each utility to 80% compliance after 2030), working out to a rate increase of about 4% to 8% for the state average, or around 6% to 18% for IOU residential rates. The cost to avoid carbon emissions is about $30-$70/tCO2.

The cost-cap under the step-wise approach projects to at least meet 90% of uncapped case even under the higher-cost scenario. This includes avoided emissions just to get to the 80% GHG-free standard that were not projected to be achieved by 2030. Incremental costs range from $600M to $1.2 billion, working out to a rate increase of about 4% to 8% for the state average, or around 26% to 27% for IOU residential rates. The cost to avoid carbon emissions is forecast to be about $40-$80/tCO2.

100% Clean Power

As reported in our prior analysis, costs become much more uncertain for eliminating the last percent of fossil fuel power generation. We have decided to keep the focus on the 99% GHG-free case because trying to parse out that last small increment is not the right question to answer in our opinion – particularly given the high uncertainty.

With robust movement to 99% GHG-free, and maintaining a “Cheap & Clean” advantage in electricity, state-wide carbon reductions can be multiplied through electrifying other end-uses. The total avoided carbon potential is many times that which would result from eliminating the last 1% of power system GHGs. Perhaps we can have both – but that remains speculative so planning without contingencies such as the cost-cap leaves ratepayers exposed.

The graph at right shows the progression of GHG reductions on a step by step basis, with percentage of state emissions reduced on the X-axis, and the cost per metric ton on the Y-axis. The step up in renewables to reach 80% GHG-free includes reliability upgrades costs, although those may be incurred prior (in the coal to natural gas switching) or after (in the expansion to 99% GHG-free) the 80% GHG-free milestone.

Note all cases come in at costs beyond the generally regarded “Social Cost of Carbon.” This data is shown in table form below:

Table 2. Case Summary (Uncapped Costs)

Appendix: Tables for 100%* Clean Power milestones (*99%)

Table A1: Avoided CO2 and costs of avoided CO2 for scenario with no cost-cap

Table A2: Avoided CO2 and costs of avoided CO2 for scenario with 2% per year cost-cap

Table A3: Avoided CO2 and costs of avoided CO2 for scenario with House amended version of cost-cap