This updated Clean & Prosperous Institute (CaPI) analysis examines the rate impacts of eliminating coal power, achieving an 80% clean energy standard by the year 2030, and a 100% clean energy standard by the year 2045. CaPI relies on a variety of sources, and deploys its own utility-specific model.

Background

The Washington State Legislature is considering Senate Bill 5116 and House Bill 1126, targeting a 100% greenhouse gas (GHG) emission-free electric sector before mid-century. These bills direct each utility to meet 80% of its annual retail load from renewable and non-emitting resources by the year 2030. If achieved, the statewide share of retail load from renewable and non-emitting resources would reach 90% (Graph 1). Each utility is also expected to eliminate coal-fired electricity by the end of 2025 or face a $60/MWh penalty, and further to reach 100% renewable and non-emitting resource portfolio by the year 2045. Combined with the 80% requirement in 2030, the elimination of coal power would decrease power sector emissions to approximately 40% of 1990 levels.

Graph 1: State % GHG-Free MWh

An 80% GHG-free resource requirement for each utility corresponds to a system wide 90% renewable and non-emitting resource portfolio.

Prior analyses have examined the system wide impact to reliability and rates across the northwest region of various clean energy standards. Using these studies as a guide, and leveraging other available sources, CaPI disaggregated multi-state data and used utility-level data to project costs and rate effects specifically for Washington state. In this process CaPI applied its own layer of assumptions, adjusting for noted concerns in previous analyses, notably greater energy efficiency deployment through at least 2030.

As provided in the Engrossed Second Substitute Senate Bill 5116 legislation, cost caps, penalty off-ramps, and reliability exemptions may limit an individual utility’s requirement to meet any of these targets. The results of this analysis are therefore helpful to understanding the likelihood of meeting the targets within those constraints.

Results

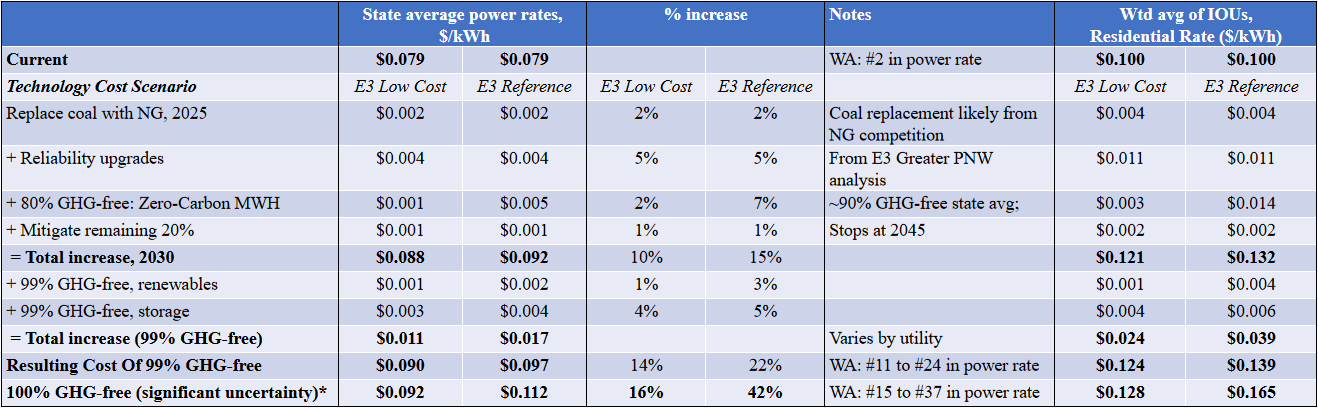

For the purpose of this analysis the aggregate state average for electric rates is assumed to be 7.9 cents per kilowatt-hour (kWh). Table 1 shows the additional steps required to achieve first 99% GHG-free, then 100% GHG-free electricity assuming an uncapped cost increase. The analysis includes both a higher cost scenario and a low cost scenario – the main difference being the pace of renewable and battery storage cost declines into the 2040s.

Our modelling suggests that achieving 99% GHG-free power by 2045 would increase costs 14% to 22% on a statewide average. Washington’s average power rates would go from 2nd lowest nationally to the between 11th and 24th, assuming no change in other states rates. For 100% clean, rates would rise more, to between 16% and 42% on a statewide basis or between 15th and 37th nationally in rates. Costs to customers of utilities with high GHG emissive generation will experience higher rate increases. For example, residential rates for the average investor owned utility (IOU) customer would nearly double the statewide average increase under an uncapped cost scenario for compliance.

At the interim target of a minimum 80% GHG-free power plus mitigation of remaining emissions, costs are projected to rise 10% to 15% on a statewide average of which 7% is from replacing coal that otherwise is not slated for closure plus building additional system reliability for integrating renewables.

*Includes CaPI factoring of 99% → 100% GHG-free case (UPDATED VALUES AND CORRECTED SUMMING ERROR FOR RIGHT TWO COLUMNS ON THE “=Total Increase (99% GHG-free)” LINE. March 5 at 7PM)

Coal Closure & Reliability Upgrades:

Enough spare natural gas capacity exists within the Pacific Northwest region to substitute completely for coal on average. Doing so means slightly higher costs, as existing coal can be run more economically absent a price on carbon than existing natural gas. Several coal closures serving 2.3 GW of “Core NW” capacity are already scheduled in the next 5-10 years, most notably 1.3 GW of Centralia capacity (Pacific Northwest Low Carbon Scenario Analysis – Technical Report). To replace an additional 2.6 GW of capacity is estimated to cost an average of 0.15 cents per kWh, concentrated over a few utilities with substantial coal resource ownership. In addition, more recent E3 analysis suggests additional natural gas combustion turbine (CT) capacity is needed to ensure high standards of system reliability, equal to 2.7 GW of new capacity (roughly 40% of projected solar capacity additions through 2030). Of this, 2.5 GW are from the three IOUs, the average impact of which is 1.1 cents per kWh. Spread across all statewide electricity load, the added cost is an additional 0.4 cents per kWh.

Minimum 80% GHG-free for each utility results in 90% at the state average:

Each utility is required to target at least 80% GHG-free electricity by 2030 or pay a compliance penalty. Since many utilities already surpass the goal, the overall system average would be 90% if this target is met by each utility (Graph 1, above). For the purpose of this analysis we assume no utility decreases its current clean percentage and there is no resource shuffling among utilities. The added cost of full compliance in 2030 is a 10% to 15% increase in statewide average rates – which includes the purchase of offsets for the remaining 10% emissive electricity. The average IOU residential customer might see rate increases double that.

Even at the increased projected rate of around $0.09/kWh, a 90% GHG-free system with no coal could fuel and electric car with one-sixth the fossil fuel emissions per mile driven at a fueling cost of less than 30% that of a 30 mpg gasoline car running on $3/gallon gasoline. Transportation emissions are the largest source of statewide emissions, so maintaining a strong price and emissions advantage provides the foundation for more rapid economy-wide decarbonization.

Breaking 100% GHG-free by 2045 into two parts: 99%, then 100%:

We split out the costs of achieving 100% in two parts because the last step has significant technological and cost uncertainty.

99% GHG-free. Load is expected to grow 21% between 2020 and 2045 (E3 2017-2018 Pacific Northwest Low Carbon Scenarios). CaPI estimated resources and costs on a utility basis to both replace emissive resources and to meet added load. Proportions of resources followed the E3 2019 Resource Adequacy in the Pacific Northwest report for the six-state “Greater Pacific Northwest” (GPNW). Table 1 separately breaks out the costs of renewables (similar amounts of solar & wind), and storage, which total a 5% to 10% additional rate increase statewide, including for IOU residential customers.

100% GHG-free. E3 projected costs of achieving 100% GHG-free electricity and system reliability for the GPNW balancing region. The graph shows progress to GHG-free emissions (X-axis) and the resulting GPNW regional costs/year (Y-axis). In the E3 scenarios, the cost jump up in the last 1%. E3 and others have shown potential pathways to lower costs. Examples include biogas, long term storage, and lower cost nuclear As E3 also eliminates the use of imports in this last step to 100% GHG-free, CaPI’s upper estimate halves the jump to a 2.5 times increase (see Section IV below). The E3 biogas scenario, on the other hand, projects costs for 100% GHG-free only incrementally higher than the reference 99% GHG-free case. This smaller proportional increase is used to factor from 99% to 100% GHG-free in the Low Cost scenario. Note there is considerable uncertainty in this estimate.

The uncapped rate increase for the three main compliance steps (2026: No coal; 2030: 80% GHG-free + mitigation of remainder; 2045: 100% GHG-free) is shown graphically, based on the information in Table 1, for both the statewide average (top) and IOUs:

Methodology for Determining State % GHG-free MWh from Utility data

Data for total MWh and MWh by type of generating resource for both claims and market. are taken from the latest Fuel Mix Disclosure for reporting year 2017. The data referenced above uses totals, the sum of both market and claimed. All coal removed is replaced by Natural Gas generation, and all Natural Gas generation is replaced by GHG-free generation in amount sufficient to meet GHG-free threshold. This is calculated on a utility-basis and then total shifts in generation are added to the state totals to determine the net impact. The analysis is based on 2017 data. At the 80% threshold for GHG-free generating resources, utilities requiring action for compliance include Avista, Clark PUD, Grant PUD, PSE, and Pacific Power. Grant PUD is included only based on market purchases while the others are under the 80% threshold on claimed resources alone. For 2017, no other utilities were under 92% GHG-free for total MWh (market purchases plus claimed resources). Franklin PUD, Klickitat PUD, and Pend Oreille PUD would require some action for compliance under a threshold that moved from 90% GHG-free requirement to 95% GHG-free requirement.

Carbon intensity is assumed to be 0.98 metric tons CO2 per megawatt-hour while natural gas resources have a carbon intensity of 0.42 metric tons CO2 per megawatt-hour (source: 2015-2017 average statewide carbon intensity by fuel based on the Department of Commerce Fuel Mix Disclosure).

Methodology and assumptions for uncapped cost of compliance

For detailed methodological steps and assumptions, we direct you to our initial analysis: https://www.cleanprosperousinstitute.org/2019/02/18/report-on-100-clean/

Since that report was posted online, we have expanded the analysis to include the low technology cost scenario. To complete that scenario, there are two main methodological departures from those in the report posted online.

Firstly, the cost to build renewable capacity is lower. Based on the 2018 Additional Scenarios capital costs in the low tech case were half of the reference case for solar, 60% of the reference case for wind, and 33% lower for battery storage. We used Lazard’s Levelized Cost of Electricity from November 2018 to estimate that 90% of solar levelized costs of electricity (LCOE) is capital cost, 80% of wind LCOE is capital, and 42% of lithium levelized storage costs is capital. These values were used to project total LCOE decreases relative to the reference scenario. Only where renewables were more expensive than natural gas alternative was an upward rate increase modelled.

Secondly, the proportional rate increase from 99% to 100% GHG-free was based on the ratio of additional costs ($/MWh) in the E3 2019 Resource Adequacy in the Pacific Northwest of the cheapest 100% pathway (with Biogas, $14-$30/MWh over the reference) to the 98% Reduction scenario resulting in 99% GHG-free ($10-$28/MWh). The result is an additional 16% additional rate increase (not 16% total rate increase) relative to the 99% GHG-free scenario.

Contact Information

David Giuliani, CaPI Chief Engineer, [email protected]

Kevin Tempest, CaPI R&D Scientist, [email protected]

Isaac Kastama, Waterstreet Public Affairs, [email protected]